When low or no interest rates are paid on deposits, with negative rates perhaps to come, there is no advantage to holding one’s money in banks rather than in cash, except for safety. With the worldwide discussion of bank “bail-ins,” that last advantage may be ephemeral. Japan offers a case study, where the public is ruining the best laid plans of mice and central bankers. From Kevin Buckland, shigeki Nozasa and Kazumi Miura at bloomberg.com:

When the Bank of Japan unexpectedly announced negative interest-rate policies in January, the first thing Tomomi Sato did was withdraw a 10th of the money in her bank account and stash it at home.

“It made me think of bank runs and shutdowns like I’ve heard there were in the past,” said the 30-something assistant to manga comic artists, who commutes for two hours from a small apartment in Tokyo’s suburbs. “Eventually, I feel like they’ll start charging me to keep my money there. When I think about that, I begin to worry.”

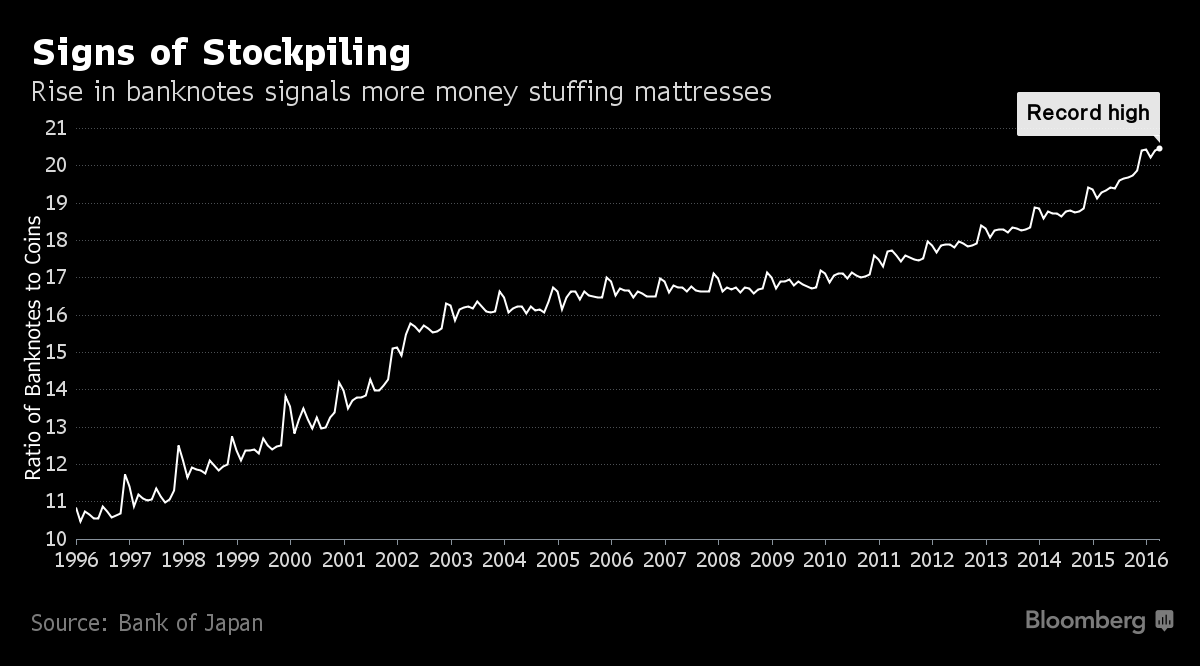

Sato is emblematic of a challenge facing the central bank that rates below zero only deepened: average Japanese aren’t feeling the benefits of more than three years of extraordinary monetary stimulus, and cash withdrawals suggest they are losing faith. About 40 trillion yen ($360 billion) has piled up in homes across Japan, according to a Dai-ichi Life Research Institute estimate — equivalent to about 8 percent of gross domestic product. That’s money banks could be lending on or using to buy bonds.

Mattress Money

“So long as Japan has what can broadly be categorized as a zero interest-rate policy, the amount will continue to grow,” said Hideo Kumano, the Tokyo-based chief economist at Dai-ichi Life and a former BOJ official. “What it means for 40 trillion yen to be sleeping under mattresses is that the deflationary mindset is deeply rooted, and Japanese have become hyper-sensitive to risk.”

https://assets.bwbx.io/images/users/iqjWHBFdfxIU/ibwm3jzGTHHM/v2/-1x-1.png

{kind=link}

Both BOJ Governor Haruhiko Kuroda and Prime Minister Shinzo Abe have highlighted the need to reinvigorate inflation expectations to spur consumption and investment. Meeting those goals has been complicated by an almost 20 percent plunge in Japanese stocks over the past year. Negative yields on Japanese government bonds maturing in up to a decade have also spurred the Ministry of Finance to cancel a string of sales aimed at retail investors.

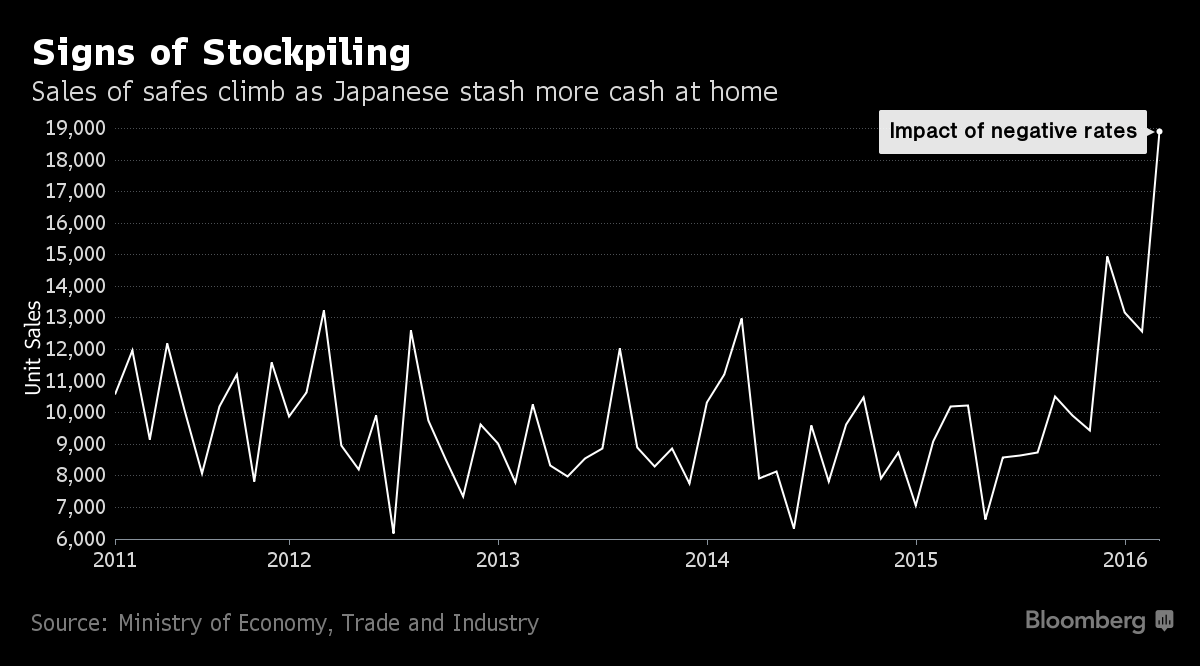

Financially, there’s little that separates the futon from a savings account that pays 0.001 percent annual interest. And perceptions that a negative deposit rate could become a tax on savers has exacerbated the migration of funds. Sales of safes in March were the highest in government data going back five years, and paper money exceeded coins in circulation by the most last month in BOJ figures to 1970.

https://assets.bwbx.io/images/users/iqjWHBFdfxIU/i5ZZB6MH9n3o/v2/-1x-1.png

{kind=link}

To continue reading: Escaping Nipponese NIRP—-8% Of GDP Has Been Stuffed Into Futons