One of the miracles of cheap credit is an improving stock price for companies whose fundamentals are deteriorating. From Wolf Richter at wolfstreet.com:

What the phenomenon of cheap credit has accomplished.

You’d think that corporate debt would grow in proportion to total sales, as this additional debt is used to fund investments in productive activities that create more sales and contribute to the economy, and that higher sales, and presumably higher earnings would create a proportionate increase in the value of the company, and thus in its stock price, and that they all go up together, not in lockstep but over time more or less at the same rate.

But that relationship between debt, sales, and share prices has gone completely out of whack.

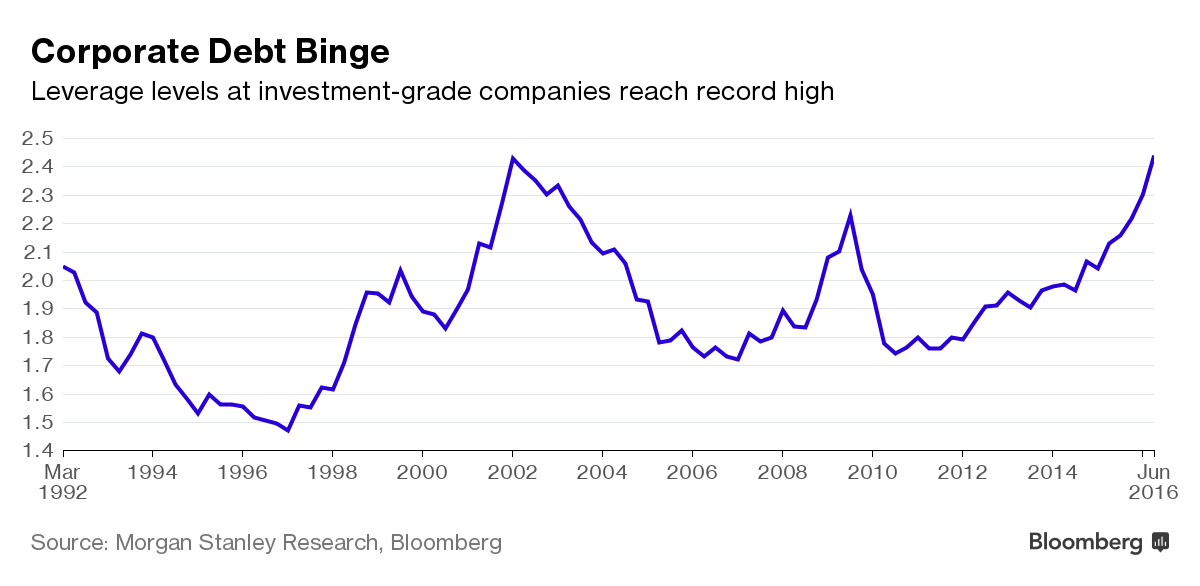

First things first: Debt at nonfinancial companies – this excludes banks and nonbank lenders such as mortgage lenders – has soared. To get a feel for just how much, I have pulled the data on three major components of corporate debt:

Bonds issued by US companies in the US. Outstanding balances never even dipped during the Financial Crisis; they only flattened for a few quarters at around $2.97 trillion. Since them, outstanding bonds have soared from record to record, in total 76%, to $5.2 trillion.

This does not include bonds that US companies issue in other currencies in other countries. For example, it does not include euro bonds (“reverse Yankees”) that are hot in Europe, where junk bond yields are at a ludicrously low 2.35% on average, and the high-grade yield is just above zero.

Commercial & Industrial loans fell sharply during the Financial Crisis as banks stopped lending and as demand from companies withered. After peaking in Q4 2008 at $1.56 trillion, C&I loans fell to $1.19 trillion by Q3 2010. Then they soared and started setting new records in early 2014. By October 2016, they were up 35% from the prior peak and 77% from the trough – though they have largely flat-lined since then.

To continue reading: Corporate Mirage: Debt out the Wazoo, Sales Languish, Stocks Soar

{kind=link}