Ludwig von Mises wrote Socialism: An Economic and Sociological Analysis, a small book published in 1922, which demonstrated that economic calculation in a socialist commonwealth is impossible. Of course, Mises assumed that the purpose of an economy, even a socialist one, was supposed to produce goods and services, which determined its success or failure.

Alain Besançon wasn’t an Austrian or a Misesian, but he wrote Anatomie d’un spectre: l’Économie politique du socialisme réel, also a small book the size of Mises’s own Socialism, in which he also observed that the Soviet economy couldn’t perform economic calculation; thus, the Soviet economy performed poorly, very poorly by Western standards.

The Soviet economy was wasteful and chaotic. Besançon believed that economic planning induced irrationality in the system. Terrified managers couldn’t report failing the plan, and consequently any subsequent economic planning would be even more divorced from reality than previous planning had been.

Both Besançon and Mises knew that socialism could not discover market prices. Both knew that this would lead to widespread corruption. However, Besançon realized that the state not only tolerated but also used the black market for price discovery in economic sectors critical to the regime, like defense and certain prestigious cultural and sport endeavors (Bolshoi Theatre, gymnastics, eventually hockey, etc.).

When the slaves revolt, they will seek the blood of their masters.

In 2013, a century after the establishment of the Federal Reserve, I published The Golden Pinnacle. The novel’s hero is Daniel Durand, a Wall Street banker. Chapter 27, “Fools’ Gold,” features Daniel’s testimony in 1913 before a House of Representatives subcommittee against legislation under consideration that would establish the Federal Reserve. Eleanor is Daniel’s wife and Tom and Alexander are two of his four sons. As the current banking crisis unfolds, I won’t have much to say that will add in any meaningful way to what I said in “Fools’ Gold”. Why repeat myself? Perhaps I’ll just keep linking back to this post. Please share in whole or in part with attribution and a link back to this post.

From “Fools’ Gold”

Daniel sat at a table in a committee hearing room of the House of Representatives. The drafts crisscrossing the room carried the winter cold of February. There were few spectators in the gallery. Daniel glanced at Eleanor, who sat with Tom and Alexander, but she was staring in a different direction. Although she had wished him well, she had seemed preoccupied when they met briefly in the hall outside the hearing room.

Members of the subcommittee of the House Committee on Banking and Currency strolled to their seats, signs denoting the representative, at an elevated, semicircular panel at the front of the room. They chatted with each other. Nine representatives sat down. The chair for Representative Bulkley of Ohio remained empty. The chairman of the subcommittee, Representative Carter Glass, from Virginia, banged his gavel.

“The hearing in consideration of House Bill 7837, for the establishment of a federal reserve bank and the furnishing of an elastic currency, shall now come to order. The subcommittee will hear the testimony of Mr. Daniel Durand, from the firm of Durand & Woodbury, of New York.” Chairman Glass’s accent had an unmistakable Virginia lilt that reminded Daniel of Aldus Kincaid, his attorney for the court of inquiry. A dapper gentleman in his mid-fifties, Glass had prominent ears and a nose that filled a larger proportion of his face than the average nose filled of the average face.

“Thank you, Mr. Chairman, and thank you, members of the committee,” Daniel said. “This legislation is still in its early stages and the details of the reserve system are the subjects of dispute. However, before everyone is enmeshed in them, it’s time to consider not just the purported benefits but also the real dangers of central banking and government-created money, or an elastic currency, if you will, and to ask if this supposed innovation is in the best interests of our country.” He glanced at his notes.

“A persistent misnomer is the term ‘bank deposit,’ which is not a deposit at all. If I take an item to a warehouse and pay a fee to deposit it for safekeeping, when I exercise my contractual rights and claim it, the owner of the warehouse must give it back to me. The owner can’t lend it out, use it to secure a loan, or give it to another depositor to satisfy his claim. On the other hand, when I put my money in a bank, the banker can lend or invest it, use those loans and investments as collateral to borrow money, or use my funds to pay creditors or other depositors. I haven’t deposited my money in the same sense that I deposited the item at the warehouse.

“My deposit is actually a loan and I’m an unsecured creditor of the bank. Much of the instability of the present system stems from a fiction. The respectable bank is housed in a neoclassical fortress and prominently displays a sturdy vault, to convince the depositor his money is safe. In fact, almost all his money leaves the bank in search of a return higher than the interest the bank pays him. Only a small portion is held in reserve to meet depositor withdrawals, although all depositors are told they can withdraw their money on demand.

“The bank has made a promise that it can’t always keep. Business and financial cycles are as immutable as human nature. When famine follows feast and fear replaces greed, the demand for money inevitably increases. The banker faces his worst nightmare—a run on the bank. Banks with sufficient reserves or borrowing power survive. Those without them go bankrupt.”

Daniel looked up at the representatives. Only a couple appeared interested.

To his credit, David Stockman was one of the few who had a clue in the 2008-2009 crisis. No surprise, he’s demonstrating that he’s up to speed on this one as well. From Stockman at internationalman.com:

Why would you throw-in the towel now? We are referring to the Fed’s belated battle against inflation, which evidences few signs of having been successful.

Yet that’s what the entitled herd on Wall Street is loudly demanding. As usual, they want the stock indexes to start going back up after an extended drought and are using the purported “financial crisis” among smaller banks as the pretext.

Well, no, there isn’t any preventable crisis in the small banking sector. As we have demonstrated with respect to SVB and Signature Bank, and these are only the tip of the iceberg, the reckless cowboys who were running these institutions put their uninsured depositors at risk, and both should now be getting their just deserts.

To wit, executive stock options in the sector have plunged or become worthless, and that’s exactly the way capitalism is supposed to work. Likewise, on an honest free market their negligent large depositors should be losing their shirts, too.

After all, who ever told the latter that they were guaranteed 100 cents on the dollar by Uncle Sam? So it was their job, not the responsibility of the state, to look out for the safety of their money.

If the American people actually wanted the big boys bailed out, the Congress has had decades since at least the savings and loan crisis back in the 1980s to legislate a safety net for all depositors. But it didn’t for the good reason that 100% deposit guarantees would be a sure-fire recipe for reckless speculation by bankers on the asset-side of their balance sheets; and also because there was no consensus to put taxpayers in harms’ way in behalf of the working cash of Fortune 500 companies, smaller businesses, hedge funds, affluent depositors and an assortment of Silicon Valley VCs, founders, start-ups and billionaires, among countless others of the undeserving.

Actually, American capitalism broke down long ago. However, the days are numbered for what’s left of it. From Tyler Durden at zerohedge.com:

In contrast to billionaire Bill Ackman’s praise for the federal government’s bailout of SVB depositors, Citadel founder Bill Griffin is not impressed, telling The FT that this action by US regulators shows American capitalism is “breaking down before our eyes”.

As a reminder, the FDIC’s Deposit Insurance Fund normally guarantees up to $250,000 in deposits, which protects small retail customers including mom-and-pop businesses. Banks pay for this guarantee with insurance premiums, but the insurance fund isn’t intended to backstop deposits of bigger customers with more capacity to weather losses if a bank goes under.

Yet, as The Wall Street Journal’s Editorial Board remarks, after venture capitalists (Democratic donors) and Silicon Valley politicians howled, the FDIC on Sunday announced it would cover uninsured deposits at SVB and Signature Bank under its “systemic risk” exception.

Apparently, Silicon Valley investors and startups are too big to lose money when they take risks. They benefited enormously from the Fed’s pandemic liquidity hose, which caused SVB’s deposits to double between 2020 and 2021. SVB paid interest of up to 5.28% on large deposits, which it used to fund loans to startups.

But now the FDIC is guaranteeing a risk-free return for startups and their investors.

Uninsured deposits normally take a 10% to 15% hair cut during a bank failure. Some 85% to 90% of SVB’s $173 billion in deposits are uninsured. The cost of this guarantee could be $15 billion.

The White House says special assessments will be levied on banks to recoup these losses.

That means bank customers with less than $250,000 in deposits will indirectly pay for this through higher bank fees. In other words, this is an income transfer from average Americans to deep-pocketed investors.

Like or hate Warren Buffet, he’s a pretty fair investor from whom a thing or two can probably be learned. From Tyler Durden at zerohedge.com:

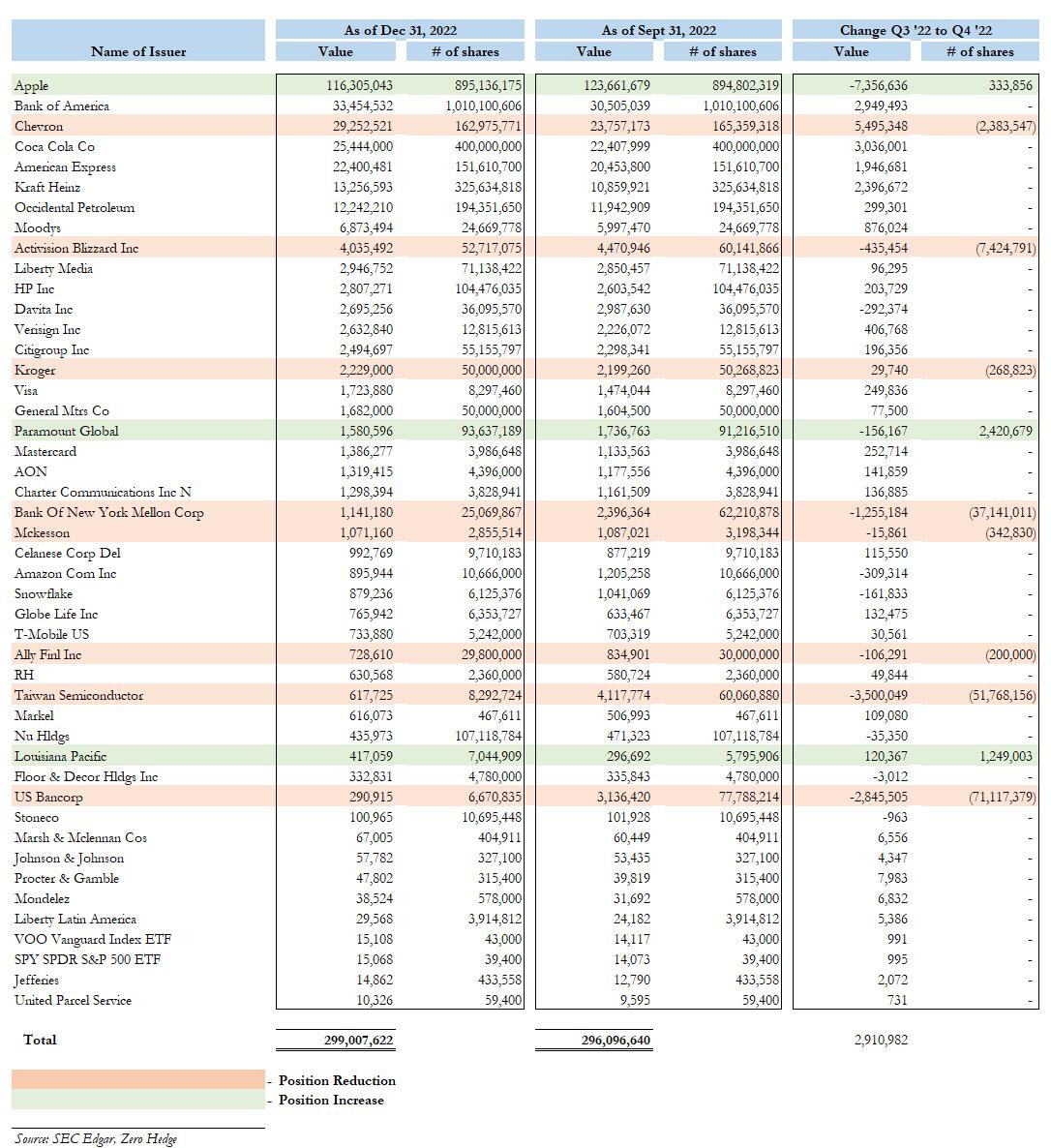

Many were wondering if Warren Buffett would address his recent unwind of Berkshire’s $4+ billion stake in Taiwan Semi – a brand new position that had catapulted into the investing conglomerate’s Top 10 holdings as of Sept 30 ’22 only to see it slashed by 86% just one quarter later…

So what did Buffett talk about in his latest and – at just barely 9 pages – shortest ever letter since Berkshire launched the practice of recapping his investment principles, activities and results some 46 years ago in 1977? Nothing that he hasn’t addressed on countless previous occasions. Below we summarize some of the key highlights.

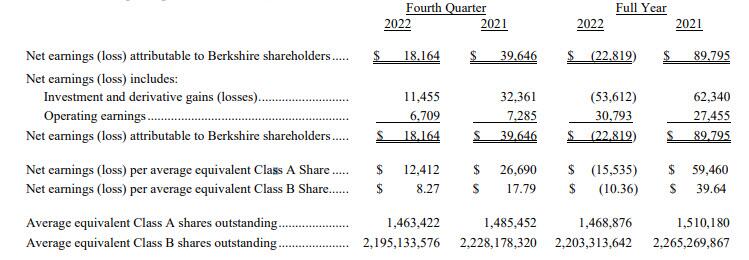

Q4 profit fell, reflecting lower gains from investments and foreign currency exchange losses as the U.S. dollar lost value. Quarterly net income fell 54% to $18.16 billion, or $12,412 per Class A share, from $39.65 billion, or $26,690 per share, a year earlier.

Of course, as is well-known, Buffett despises GAAP earnings and instead urges investors to look at operating earnings instead which strip away the quarterly fluctuations of the conglomerate’s public stock investments (i.e. unrealized gains/losses).

The GAAP earnings are 100% misleading when viewed quarterly or even annually. Capital gains, to be sure, have been hugely important to Berkshire over past decades, and we expect them to be meaningfully positive in future decades. But their quarter-by-quarter gyrations, regularly and mindlessly headlined by media, totally misinform investors.

There’s not an important area of the economy into which the government does not meddle, which means those areas are mixed economy, not capitalist. Nowhere is this more evident than in banking. From Ryan McMaken at mises.org:

It’s a sure bet that as the economy worsens, unemployment surges, foreclosures rise, defaults climb, and economic misery ensues, we’ll be told it’s all capitalism’s fault. The question one must ask, however, is, “What capitalism?”

The claim that “too much” capitalism drives every economic calamity is standard among anticapitalists on both the left and the right. They have many bullet points claiming government programs and government spending are everywhere retreating while free-market capitalism is experiencing a resurgence. This can be easily shown to be empirically false. Evidence can be found in everything from the continual flood of government regulations to rising per capita taxation and spending to the growing army of government employees. That’s all in the United States, mind you, the supposed headquarters of “free-market capitalism.” We might also point to how the US welfare state, including the immense amounts of government spending on healthcare and pensions, is on a par with European welfare states in terms of size. The supposed lack of social benefits programs in the US has long been a myth. The trend in spending, taxation, and regulation is unambiguously upward.

In recent years, though, one additional indictor of just how little capitalism is actually going on has surfaced: central banks around the world are buying up huge amounts of financial assets in order to subsidize certain industries, inflate prices, and generally manipulate the economy. This is certainly true of the American central bank, the Federal Reserve.

How the Federal Reserve Came to Dominate Financial Asset Markets

While the Fed has long bought government debt in its so-called open-market operations to manipulate the interest rate, wholesale buying of financial assets began in 2008. This included both US government Treasurys and—in a new development—private-sector mortgage-backed securities (MBSs). This was done to prop up banks and other firms that had bet on the lie that “home prices always go up.” The value of mortgage-backed securities was falling fast, so beginning in 2008, the Fed bought up MBSs to the tune of $1.7 trillion. That was all before covid.

The world reached an apex of freedom in the United States during the Industrial Revolution.The Golden Pinnacle is a novel by Robert Gore that celebrates that time. I would cut off the period at 1913, when the income tax amendment was ratified and the Federal Reserve instituted. From Jacob G. Hornberger at fff.org:

My favorite period of history is the United States in the years 1870-1915.

Why?

Because it is the freest period in the history of man.

Was it a libertarian panacea? Nope. There were, in fact, infringements on liberty, such as the violation of women’s rights, the Sherman Antitrust Act of 1870, compulsory school-attendance laws in Massachusetts, and others.

But in terms of economic liberty, there is nothing that can match it.

Imagine:

No income taxation or IRS. People were free to keep everything they earned.

No welfare, including Social Security and Medicare. Charity was entirely voluntary.

No drug laws. People were free to consume, possess, or distribute whatever they wanted.

No immigration controls. Everyone was free to come to the United States.

No minimum-wage laws.

Very few economic regulations. Economic enterprise was free of governmental control.

No foreign wars, interventions, wars of aggression, coups, state-sponsored assassinations, torture, or indefinite detention, except, unfortunately, the Spanish-American War in 1898 and the war against the Filipino people, which signaled the turn toward empire.

The pilgrims didn’t have much to be thankful for until they discovered that capitalism and free markets work well. From Thomas DiLorenzo at lewrockwell.com:

In recent years the unhinged Marxist Left in “higher” education along with the hard-Left pop communists in the teachers’ unions have been preaching that Thanksgiving is a celebration of genocide, mass murder, and imperialism. The Pilgrims murdered all the Indians, they say, and then sat down and treated themselves to big feast to celebrate their feat. They even invented the elementary schoolish word “Thankskilling” to describe it. (Send your kid to a university and he, too, can learn to sound like an uneducated Marxist moron for the rest of his life).

In reality, if the Pilgrims had anything to celebrate it was the destruction of an early form of socialism that allowed them to survive and prosper. When the first settlers arrived in Jamestown, Virginia in May of 1607 they found incredibly fertile soil and a cornucopia of seafood, wild game, and fruits of all kinds. Nevertheless, within six months all but 38 of the original 104 Jamestown settlers had starved to death. Two years later the Virginia Company sent 500 more settlers and within six months 440 of them were dead by starvation and disease. This became known as “the starving time.” The Massachusetts Pilgrims fared no better. About half of the 101 people who arrived on Cape Cod in November of 1620 were dead within a few months.

In 1611 the British government sent Sir Thomas Dale to serve as the “high marshal” of the Virginia colony. He immediately recognized the problem: The Virginia Company had adopted a system of agricultural socialism under which everything grown or produced would go to a “common store” and divided equally among all the family groups. The man who worked hard sixteen hours a day would be given the same remuneration as the man who did not work at all. Dale’s solution was to establish property rights by allotting three acres of land to each man, who was still required to pay a fee to the Virginia colony (most early American immigrants were indentured servants) but then could keep everything else for himself and his family.

Bitcoin embodies the promise of encryption, a way to free yourself from government. From Paul Rosenberg at freemansperspective.com:

Over the past few years, huge numbers of people have come to see Bitcoin as an investment… as a stock. That’s because a significant percentage of the populace – certainly a good percentage of the investing class – knows someone, at least a friend of a friend, who has done very well with Bitcoin. That’s the kind of thing that people notice, and not unreasonably so.

The truth, however, is that Bitcoin is more and better than an investment… much more and much better.

We’ll get to some detail on this later, but before I start on the story of Bitcoin, I should at least say that rather than being an investment (even though its exchange price does rise dramatically), Bitcoin is actually a new societal model. It is fundamentally different from the old model, being both more efficient and morally superior.

It Came From Outside

Now, let’s spend a few minutes on where this thing came from. And the short version is that it came from outside.

Bitcoin, you see, is not an adaptation based on existing currencies, nor can it be understood that way. Bitcoin is from the realm of radicals.

In particular, Bitcoin came to us from the cypherpunks, a group of cryptography advocates. They began to flourish in the early 1990s, as they realized they could “wall-off” areas of cyberspace from the intrusions of governments. Here, to give you some flavor, are a few quotes from these people:

Governments of the Industrial World, you weary giants of flesh and steel, I come from Cyberspace, the new home of Mind. On behalf of the future, I ask you of the past to leave us alone. You are not welcome among us.

We don’t much care if you don’t approve of the software we write. We know that software can’t be destroyed and that a widely dispersed system can’t be shut down.

A specter is haunting the modern world, the specter of crypto anarchy.

Arise, you have nothing to lose but your barbed wire fences!

We may have to wait for Laissez-Faire until after economic collapse, but after such a collapse, what else can you try? From Mark Thornton at mises.org:

My previous article demonstrated how the free market solves a boom-bust crisis and is the only solution, its effectiveness depending upon the magnitude of the crisis and, more importantly, how much the government intervenes in response. The bigger the problem created by the Fed, the greater the crisis and the more government intervenes, and the slower the economy recovers.

Here we consider how the market works most effectively, with the efficiency of the process maximized by policy restraint. Like most illnesses, recessions can be “cured” with rest, hydration, nutrition, and fresh air, rather than major surgeries and dangerous medications.

The solution begins with getting rid of the initial monetary causes and allowing market participants, especially entrepreneurs, to adjust to the new conditions. Entrepreneurs will reallocate resources according to current consumer preferences and away from the previous policy allocations. There is no easy, straightforward market playbook for an individual entrepreneur to consult. Should a pizza restaurant stay open one hour later or use in-house delivery drivers? The owner could figure it out, but policy makers would have no idea of where to even begin to answer such questions.

{kind=link}

{kind=link}

{kind=link}